Atlantic Handysizes are presently outperforming their eastern counterparts insofar as their rates are holding to last-done and not coming under the kind of pressure being seen in Southeast Asia. As such, northbound trips from Southeast Asia to Singapore-Japan on tonnage of 38-42,000 dwt have slipped into the US$ 11,000s after trading in the low US$ 12,000s in early December. The inter-Atlantic trips (UKC-Med to USEC, for example) are holding steady in the higher US$ 8,000s and lower US$ 9,000s on tonnage of 48,000 dwt. One 2011-built vessel of 57,000 dwt open Mumbai is said to have fixed US$ 9,500-9,750 daily from Mina Saqr to AG-EC India. (For news & updates on dry bulk shipbroking, subscribe to the BMTI Daily Report.)

Atlantic Handysizes are presently outperforming their eastern counterparts insofar as their rates are holding to last-done and not coming under the kind of pressure being seen in Southeast Asia. As such, northbound trips from Southeast Asia to Singapore-Japan on tonnage of 38-42,000 dwt have slipped into the US$ 11,000s after trading in the low US$ 12,000s in early December. The inter-Atlantic trips (UKC-Med to USEC, for example) are holding steady in the higher US$ 8,000s and lower US$ 9,000s on tonnage of 48,000 dwt. One 2011-built vessel of 57,000 dwt open Mumbai is said to have fixed US$ 9,500-9,750 daily from Mina Saqr to AG-EC India. (For news & updates on dry bulk shipbroking, subscribe to the BMTI Daily Report.)

Panamax spot markets have endured another week of steady pressure and lower rates with the relative strength in new activity across the Atlantic still lending little, if any, support to long haul freight levels. Inter-Atlantic Kamsarmax trips (basis 82,000 dwt) have been securing upwards of US$ 11,500 from the Continent to the USG, though owners say such business has been sporadic at best. Pacific activity has been spotty with owners settling for around US$ 11,000 on NoPac round voyages. (For news & updates on dry bulk shipbroking, subscribe to the BMTI Daily Report.)

Panamax spot markets have endured another week of steady pressure and lower rates with the relative strength in new activity across the Atlantic still lending little, if any, support to long haul freight levels. Inter-Atlantic Kamsarmax trips (basis 82,000 dwt) have been securing upwards of US$ 11,500 from the Continent to the USG, though owners say such business has been sporadic at best. Pacific activity has been spotty with owners settling for around US$ 11,000 on NoPac round voyages. (For news & updates on dry bulk shipbroking, subscribe to the BMTI Daily Report.)

Recent days of consecutive gains for the Capesizes have pushed rates back up to near their YTD peaks of the early summer. Chartering activity was buoyed by steady and growing cargo demand in both hemispheres, seemingly unhindered by the loss of broking players from the magnet effect of the Eisbein weekend in Hamburg. Adverse weather conditions have been tying up vessels across several big Pacific runs, adding to the tightening in available tonnage, making charterers scramble even more for ships as cargo requirements grow apace. Inter-Pacific voyage rates have surged over the past week with W.Australia delivery to S.China reaching upwards of US$ 9.8/mt after trading at around US$ 8.6/mt just a week earlier. In the western hemisphere, trans-Atlantic RVs have surged nearly US$ 2,000 day-by-day to push levels back to the high teens of US$ 18,000. Front haul trips have pushed past US$ 40,000 daily.

Recent days of consecutive gains for the Capesizes have pushed rates back up to near their YTD peaks of the early summer. Chartering activity was buoyed by steady and growing cargo demand in both hemispheres, seemingly unhindered by the loss of broking players from the magnet effect of the Eisbein weekend in Hamburg. Adverse weather conditions have been tying up vessels across several big Pacific runs, adding to the tightening in available tonnage, making charterers scramble even more for ships as cargo requirements grow apace. Inter-Pacific voyage rates have surged over the past week with W.Australia delivery to S.China reaching upwards of US$ 9.8/mt after trading at around US$ 8.6/mt just a week earlier. In the western hemisphere, trans-Atlantic RVs have surged nearly US$ 2,000 day-by-day to push levels back to the high teens of US$ 18,000. Front haul trips have pushed past US$ 40,000 daily.

For exclusive news and updates about dry bulk shipbroking, subscribe to the BMTI Daily Report.

Atlantic Ultramaxes are buoyed by the success of the USG delivery business with front hauls pushing steadily toward US$ 25,000 daily on modern tonnage of 63,500 dwt bound for the Far East. Spot rates for Black Sea front hauls have also climbed over US$ 20,000 daily for the first time this month and shipowners believe there is still plenty more upside to potential go. Handysize vessels have also been faring well in the Atlantic with positive movement in rates from NCSA to the Continent moving into the US$ 15,000s on tonnage of 38-42,000 dwt. Inter-Pacific Handysizes continue to trade in the US$ 14,000s.

Atlantic Ultramaxes are buoyed by the success of the USG delivery business with front hauls pushing steadily toward US$ 25,000 daily on modern tonnage of 63,500 dwt bound for the Far East. Spot rates for Black Sea front hauls have also climbed over US$ 20,000 daily for the first time this month and shipowners believe there is still plenty more upside to potential go. Handysize vessels have also been faring well in the Atlantic with positive movement in rates from NCSA to the Continent moving into the US$ 15,000s on tonnage of 38-42,000 dwt. Inter-Pacific Handysizes continue to trade in the US$ 14,000s.

For exclusive news and updates about dry bulk shipbroking, subscribe to the BMTI Daily Report.

Greek Med: Steady cargoes are keeping steady rates in the area. Corn cargoes of 3,000mt (51′) are fixing rates of US$24-25/mt from Izmail to Patras, brokers say. Grain of 5,000mt (49′) from the Odessa area can fetch US$ 24-25/mt to WC Greece while the same cargo from Reni to EC Greece can get US$ 22/mt. Turkish Med: Grain cargoes of 5,000mt (54′) from the Danube River (ex-Reni) are securing upwards of US$ 24/mt to Mersin and, according to shipbrokers, US$ 25/mt to Iskenderun. Soybean cargoes of 6,000 (52′) from Chornomorsk have been actively getting chartered to Iskenderun in the US$ 19-21/mt range. Adriatic Sea: Rebar of 3,000mt was fetching upwards of US$ 17-18/mt ex-Icdas to Durres in the last days of September. Minerals of 4,500mt are being concluded on urgent terms at US$ 31/mt ex-Tuapse to Koper, owners report. Grain of 5,000mt (46′) did US$ 29.5/mt ex-Galatz to Italian Adriatic. Grain for Split/Bari business is fetching US$ 12/mt.

Greek Med: Steady cargoes are keeping steady rates in the area. Corn cargoes of 3,000mt (51′) are fixing rates of US$24-25/mt from Izmail to Patras, brokers say. Grain of 5,000mt (49′) from the Odessa area can fetch US$ 24-25/mt to WC Greece while the same cargo from Reni to EC Greece can get US$ 22/mt. Turkish Med: Grain cargoes of 5,000mt (54′) from the Danube River (ex-Reni) are securing upwards of US$ 24/mt to Mersin and, according to shipbrokers, US$ 25/mt to Iskenderun. Soybean cargoes of 6,000 (52′) from Chornomorsk have been actively getting chartered to Iskenderun in the US$ 19-21/mt range. Adriatic Sea: Rebar of 3,000mt was fetching upwards of US$ 17-18/mt ex-Icdas to Durres in the last days of September. Minerals of 4,500mt are being concluded on urgent terms at US$ 31/mt ex-Tuapse to Koper, owners report. Grain of 5,000mt (46′) did US$ 29.5/mt ex-Galatz to Italian Adriatic. Grain for Split/Bari business is fetching US$ 12/mt.

Subscribe to the BMTI Short Sea Report today for exclusive news on the European Short Sea markets.

The newfound strength of eastern Panamaxes has yet to ripple through the entire sector, though Pac-based Panamaxes are still building steam with RVs on 82,000 dwt now trading just below US$ 14,000 daily with US$ 15,000 levels in negotiations for the beginning of next week. Atlantic rates are less enthusiastic at the moment as front hauls on Kamsarmaxes refuse to rise much higher than US$ 21,000 daily.

The newfound strength of eastern Panamaxes has yet to ripple through the entire sector, though Pac-based Panamaxes are still building steam with RVs on 82,000 dwt now trading just below US$ 14,000 daily with US$ 15,000 levels in negotiations for the beginning of next week. Atlantic rates are less enthusiastic at the moment as front hauls on Kamsarmaxes refuse to rise much higher than US$ 21,000 daily.

For exclusive news and updates about dry bulk shipbroking, subscribe to the BMTI Daily Report.

Freights are climbing again in the southern European trades to the delight of owners working in the area and running against the prevailing summer holidays of northern Europe. Freights for grain ex-Rostov to Marmara are up to US$ 26/mt while grain ex-Rostov to the Egyptian Med is up to US$ 42-43/mt, depending on terms (basis grain of 5,000mt). Owners are seeking higher rates on grains from Danube River ports as well with grain cargoes from Reni now fetching US$ 17/mt and even US$ 18/mt to the Sea of Marmara (stowage of 53′) on 5,000mt. Grain ex-Reni to the Italian Adriatic has been fetching rates of US$ 26/mt, brokers report. Danube freights are nonetheless far below their levels of one year ago, owners note, when Reni/Marmara trades were up to US$ 42/mt (now securing less than half of this).

Subscribe to the BMTI Short Sea Report today for exclusive news on the European Short Sea markets.

Even with the stabilizing trends of early July having comforted owners about their summer prospects, overall cargo demand continues to wane inexorably across the European coaster trades. Week-on-week discounts have been manageable, but they are discounts nonetheless and owners could be dealing with some serious cumulative discounts by the time holiday season is through. Northbound trips from the North of Spain to Ireland are still fetching middle EUR 20s/mt of EUR 25/mt, depending on terms, though charterers have been having some success in slowly moving that range downward over the course of the month so far. Southbound trips remain comparatively more lucrative with talk of EUR 50s/mt still being fixed on the more urgent trades from SCUK to the Turkish Med. Other sources say high EUR 40s/mt are the best that an owner could hope for on this run in the current spot market. Steady-to-slumping bunker prices have not given owners any leverage in negotiations either, leaving them with little recourse but to take what the charterers are offering.

Even with the stabilizing trends of early July having comforted owners about their summer prospects, overall cargo demand continues to wane inexorably across the European coaster trades. Week-on-week discounts have been manageable, but they are discounts nonetheless and owners could be dealing with some serious cumulative discounts by the time holiday season is through. Northbound trips from the North of Spain to Ireland are still fetching middle EUR 20s/mt of EUR 25/mt, depending on terms, though charterers have been having some success in slowly moving that range downward over the course of the month so far. Southbound trips remain comparatively more lucrative with talk of EUR 50s/mt still being fixed on the more urgent trades from SCUK to the Turkish Med. Other sources say high EUR 40s/mt are the best that an owner could hope for on this run in the current spot market. Steady-to-slumping bunker prices have not given owners any leverage in negotiations either, leaving them with little recourse but to take what the charterers are offering.

The chartering market within the Atlantic remains a mixed bag of opportunities. Baltic-Black Sea range not overly amusing whilst USG-W.Africa and, obviously, the ECSA seem the better areas to be, though a softening trend seems slowly becoming more evident. Off the Continent, Supra chars were shrugging their shoulders when they were seeing tonnage at US$ 25,000 for a quick eight-day employment from GNS to the Netherlands, for which trade realistic owns were coming up with US$ 12,500 daily. Scrap charterers were discussing 58,000 dwt at US$ 10-11,000 daily for a trip from GNS to eastern Med. Steel charterers were rating 53,000 dwt tonnage at US$ 11,000 daily for a trip to USEC. Considering this, dropping a Supramax on subs at US$ 14,500 daily for similar is only logical. Trips with clinker from the West Mediterranean to West Africa are down to US$ 13,500 daily on Ultramax tonnage. Continue reading

The chartering market within the Atlantic remains a mixed bag of opportunities. Baltic-Black Sea range not overly amusing whilst USG-W.Africa and, obviously, the ECSA seem the better areas to be, though a softening trend seems slowly becoming more evident. Off the Continent, Supra chars were shrugging their shoulders when they were seeing tonnage at US$ 25,000 for a quick eight-day employment from GNS to the Netherlands, for which trade realistic owns were coming up with US$ 12,500 daily. Scrap charterers were discussing 58,000 dwt at US$ 10-11,000 daily for a trip from GNS to eastern Med. Steel charterers were rating 53,000 dwt tonnage at US$ 11,000 daily for a trip to USEC. Considering this, dropping a Supramax on subs at US$ 14,500 daily for similar is only logical. Trips with clinker from the West Mediterranean to West Africa are down to US$ 13,500 daily on Ultramax tonnage. Continue reading

Capesize freights look like they might already be getting re-energized a la last week with front hauls swiftly returning to the psychologically powerful US$ 50,000 daily line and Pacific RVs bounding over US$ 26,000 daily. Trans-Atlantic RVs are still moving sideways in the US$ 21,000s, but owners say they expect things to start recovering there as well if the jump in front hauls is any indication of things to come. China/Brazil RV freights are also holding to unchanged levels in the US$ 25,000s.

Capesize freights look like they might already be getting re-energized a la last week with front hauls swiftly returning to the psychologically powerful US$ 50,000 daily line and Pacific RVs bounding over US$ 26,000 daily. Trans-Atlantic RVs are still moving sideways in the US$ 21,000s, but owners say they expect things to start recovering there as well if the jump in front hauls is any indication of things to come. China/Brazil RV freights are also holding to unchanged levels in the US$ 25,000s.

Warmer conditions in the last two weeks of May helped alleviate some of the wet conditions that were plaguing French wheat crops following a rainy growing season, but returning showers in the final days of the month renewed concerns about the French grain crop. French farm office, FranceAgriMer, says domestic wheat conditions remain at four-year lows with some 63% of the country’s soft wheat currently rated as good or excellent versus 93% with the same rating one year ago (and down slightly from the 64% recorded one week ago). The good-to-excellent rating for French durum wheat was 64% (compared to 66% for the same a week earlier).

Warmer conditions in the last two weeks of May helped alleviate some of the wet conditions that were plaguing French wheat crops following a rainy growing season, but returning showers in the final days of the month renewed concerns about the French grain crop. French farm office, FranceAgriMer, says domestic wheat conditions remain at four-year lows with some 63% of the country’s soft wheat currently rated as good or excellent versus 93% with the same rating one year ago (and down slightly from the 64% recorded one week ago). The good-to-excellent rating for French durum wheat was 64% (compared to 66% for the same a week earlier).

No safety net is evident for the Capesizes at present with freights falling steadily on long haul trades in the Atlantic (if less so in the Pacific). Front haul rates based on UKC delivery have slipped into the US$ 48,000s with charterers already heard to be seeking US$ 46,000 daily for end-month positions for willing owners. While this currently bearish turn is far from disastrous, owners are hoping the tides will turn back into their favour sooner rather than later.

No safety net is evident for the Capesizes at present with freights falling steadily on long haul trades in the Atlantic (if less so in the Pacific). Front haul rates based on UKC delivery have slipped into the US$ 48,000s with charterers already heard to be seeking US$ 46,000 daily for end-month positions for willing owners. While this currently bearish turn is far from disastrous, owners are hoping the tides will turn back into their favour sooner rather than later.

Capesizes enjoy a new upswing in demand with the eastern basin looking especially improved thanks to new orders being made for early May positions and trans-Pacific RVs climbing up past the US$ 26,000 marker. Owners are hoping that momentum will continue into the end of the week and potentially even push these freights into the high US$ 20,000s or even US$ 30,000 by the weekend. Front hauls are edging upwards in the US$ 40,000s to US$ 46,000 daily.

Eastern Supramaxes have seen choppier waters of late with rates for NoPac rounds moving largely sideways in the US$ 14,000s on tonnage of 58,000 dwt and the US$ 16,000s for Ultras of 62-63,000 dwt. Black Sea front hauls, meanwhile, have started to bounce back to prior highs with more Supra owners seeing rates in the US$ 26-27,000 range instead of the US$ 25-26,000 range of a week before. Volatility is back in the Atlantic with APS rates for cement from Turkish Med to USG on 58,000 dwt ships said to have been done at everything from US$ 12,250 daily plus US$ 170,000 BB to US$ 15,250 daily plus US$ 175,000 BB (ILOHC). Another 2010-built 58,000 dwt is said to be on subs from South Africa to WCI at US$ 18,000 daily plus US$ 180,000 BB (or if ECI at US$19,000 daily plus US$ 190,000 BB).

For exclusive news and updates about dry bulk shipbroking, subscribe to the BMTI Daily Report.

The holding pattern continues for Capesizes as markets enter the middle of the Golden Week with only mild buoyancy seen in front hauls. Standard front haul freights are hovering in the low US$ 40,000s with the best-positioned tonnage fetching as much as US$ 43,000 on modern vessels of 180,000 dwt based on S’pore-Japan redel. Inter-Pac round voyage rates persist in trading just below US$ 20,000 daily.

The holding pattern continues for Capesizes as markets enter the middle of the Golden Week with only mild buoyancy seen in front hauls. Standard front haul freights are hovering in the low US$ 40,000s with the best-positioned tonnage fetching as much as US$ 43,000 on modern vessels of 180,000 dwt based on S’pore-Japan redel. Inter-Pac round voyage rates persist in trading just below US$ 20,000 daily.

Panamax freights have not collapsed as many feared they may do this week, although they are not flying to new highs either. By the same token, shipbrokers note, they have been picking up some US$ 200 dependably day-on-day over the past few days, which has seen TARV rates creep up toward US$ 15,000 daily on modern tonnage of 82,000 dwt and US$ 14,000 daily on standard vessels of 74-76,000 dwt.

Ultramax rates are losing some traction in the Black Sea with delivery from the area a bit less complicated as it was a week ago with avails back then proving harder to get for charterers looking to capitalize on the fluctuating grain market. At present, front haul rates ex-Black Sea are still giving high US$ 20,000s at up to US$ 29,000 daily but not very much higher.

For exclusive news and updates about dry bulk shipbroking, subscribe to the BMTI Daily Report.

Globally, grain prices appear to be trending gradually upward with the UN’s FAO Cereal Price Index—which tracks world prices for wheat, maize, rice and barley—up by 1.5% in November from the month before, although it is notable that the 2023 average level for the same index was 15.4% below the 2022 average (albeit a year with historically elevated commodity prices). European Union soft wheat production is predicted by Strategie Grains to fall slightly by 1% YoY in 2024 to 124.8 Mt (from 2023’s 125.9 Mt). On the other hand, the analysts expect to see EU barley output to rise by 11% YoY this year to 52.7 Mt (despite a 0.8% YoY drop in winter barley sowings). The European Commission recently raised its forecast for usable production of EU maize for the 2023/24 season to 61.4 Mt (from an earlier 59.9 Mt made a month prior). This would be 15.6% above the previous season’s output, a period in which drought conditions adversely affected much of the EU maize crop, but nonetheless still 10.8% below the five-year average.

Pressure has been notable on Supramax spot freights over the past week even as trends have not been as uniformly deflationary as in other markets with average inter-Pacific rates losing around US$ 500 week-on-week. Current NoPac rounds for 58,000 dwt ships, for instance, are now trading within the high US$ 10,000s daily range in contrast to the lower US$ 11,000s as seen a week earlier during the most recent course correction. Short period deals on Ultramax vessels are still looking rather robust with 3-5 months being secured in excess of US$ 16,500 daily.

Pressure has been notable on Supramax spot freights over the past week even as trends have not been as uniformly deflationary as in other markets with average inter-Pacific rates losing around US$ 500 week-on-week. Current NoPac rounds for 58,000 dwt ships, for instance, are now trading within the high US$ 10,000s daily range in contrast to the lower US$ 11,000s as seen a week earlier during the most recent course correction. Short period deals on Ultramax vessels are still looking rather robust with 3-5 months being secured in excess of US$ 16,500 daily.

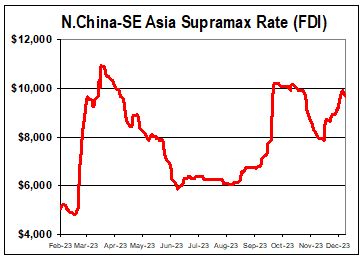

Corrections have been evident within the eastern basin Handysizes with Pacific rounds on tonnage of 38-42,000 dwt having moved downward from the upper US$ 9,000s into the lower US$ 9,000s over the past week period. Shipowners do say that they expect to see some firming in demand going into the year-end holiday period.

For exclusive news and updates about dry bulk shipbroking, subscribe to the BMTI Daily Report.

With the ever-important holiday period bearing down in the next few weeks, traders, owners and charterers alike are all looking at the writing on the wall, hoping to put in their last-minute year-ending requirements at the best possible profit. As such, market fundamentals remain locked into a largely sideways path even as there are no longer signs of bunker prices rising enough to push operating costs any higher than they were at the start of the month. Northbound trips are still fetching rates just below €50/mt from the Spanish Med into the North Sea with some reports of rates even exceeding €50/mt on redelivery Ireland. Southbound freights from Ireland into the lower Baltic are securing rates in the middle-high €20s/mt with at least one owner claiming to have fixed €30/mt on this business with agri-prods of 5,000mt (46′). Charterers are said to be behaving slightly more accommodating for fixing urgent business on Baltic delivery with the BMTI benchmark rates from the Baltic States to ARAG seen pushing slightly higher into the mid-high €20s/mt range and talk of €27-28/mt being done on some cargoes ex-Klaipeda even if the prevailing rates are still largely in the vicinity of €26/mt on this run. Stormy weather rolling across the North Sea and northern Continent is said to be getting even worse, which has driven a number of delays and cancellations, which are in turn impinging on overall tonnage availability, ultimately propping up freights by an uncertain degree.

Subscribe to the BMTI Short Sea Report today for exclusive news on the European Short Sea markets.

Following an extended period of ups and downs, Capesize rates hit the first proper week of November with a major surge of recovery. Gains have been especially notable in the Pacific where the going rates for Pac RVs have jumped by as much as US$ 4,000 in 48 hours to trading in the high teens of US$ 17-18,000 daily—no small feat considering the same rates were in the low teens just a few days before.

Atlantic Panamaxes appear to be mounting a mild recovery if the past day of trading is any indication. Owners of 82,000 dwt vessels are fetching upwards of US$ 15,000 daily at the moment when they were settling for US$ 14,000s this time a week before. New front haul trips are also edging upward ever so slowly with US$ 22-23,000 daily range rates now showing buoyancy in heading toward US$ 23,000.

There has been increased talk of a weaker feel and owners’ willingness to compromise, which does not stop the market to become an intense battle ground for tonnage in the medium and long term future. The technical challenge to meet the decarbonisation standards is one problem, but the costs involved to meet these new standards could force many owners out of business. Thus, the owning landscape could be up for a profound change. As a consequence, as outlined earlier this week, decarbonisation might lead to a temporary lack of tonnage and, as a consequence, could severely hamper global trade. At any rate, the spot market remains in good health, despite a weaker sentiment. Off the Continent, a 28,000 dwt vessel got fixed at US$ 13,500 daily for a trip to the eastern Med. Handysize freights for trips to West Africa are hovering at around US$ 18-20,000 daily.

Freights from the Sea of Azov have rocketed by as much as US$ 8/mt week-on-week due to extreme unavailability of tonnage and the associated delays in passing the Kerch Strait. Current delays are said to be averaging 8-15 days with little immediate relief in sight. Rising opex (spurred by rising bunker prices) are giving owners one more reason to hike their rate ideas from last-done going into the last quarter of the year. With Yeisk delivery to Marmara, standard grain cargoes are fetching high US$ 60s/mt of up to US$ 69/mt while Rostov delivery with the same redel is said to be trading beyond US$ 70/mt with some reports of even US$ 73-74/mt done. Danube freights remain volatile with Reni/Marmara grains in the range of US$ 40-45/mt, depending on terms. For news and trends in the European short sea markets every week, subscribe to the BMTI Short Sea Report.

After ending last week on a bit of a down note, Capesizes start the new week with something of a surprising return to positivity with stabilizing trends in the Atlantic and continued buoyancy in the Pacific. Pacific round voyage rates have been especially bullish of late with owners who had taken US$ 11,000s last week already heard to be asking charterers for US$ 12,000s on mid-September dates. Panamaxes have turned into a split market with geographically eastern rates out-performing their western counterparts. Trans-Atlantic RVs are falling by some US$ 300-400 day-on-day (into the low US$ 22,000s) while Pacific RVs are increasing by around the same amount on a daily basis to trade in the middle US$ 11,000s. Southeast Asia is thriving as well with Indo rounds moving above US$ 10,000. Supramax rates are climbing across the board thanks to a convergence of global chokepoints that are making available tonnage slightly harder to hire in both hemispheres. In the East, a 58,000 dwt vessel has secured a rate of about US$ 17,000 daily going from Madagascar to China. Short period time charters are getting concluded at upwards of US$ 15,000 daily on Handymax tonnage open in the PG-WCI area.

After ending last week on a bit of a down note, Capesizes start the new week with something of a surprising return to positivity with stabilizing trends in the Atlantic and continued buoyancy in the Pacific. Pacific round voyage rates have been especially bullish of late with owners who had taken US$ 11,000s last week already heard to be asking charterers for US$ 12,000s on mid-September dates. Panamaxes have turned into a split market with geographically eastern rates out-performing their western counterparts. Trans-Atlantic RVs are falling by some US$ 300-400 day-on-day (into the low US$ 22,000s) while Pacific RVs are increasing by around the same amount on a daily basis to trade in the middle US$ 11,000s. Southeast Asia is thriving as well with Indo rounds moving above US$ 10,000. Supramax rates are climbing across the board thanks to a convergence of global chokepoints that are making available tonnage slightly harder to hire in both hemispheres. In the East, a 58,000 dwt vessel has secured a rate of about US$ 17,000 daily going from Madagascar to China. Short period time charters are getting concluded at upwards of US$ 15,000 daily on Handymax tonnage open in the PG-WCI area.

For exclusive news and updates about dry bulk shipbroking, subscribe to the BMTI Daily Report.

Freights were generally improved over the past week among the Far East Supramaxes, holidays in Singapore and spotty activity notwithstanding, as average rates seem to have picked up around US$ 300-500 week-on-week (basis NoPac RV with tonnage of 58,000 dwt). Indeed, the inter-Pacific round voyage freights rose steadily from the middle US$ 6,000s to nearly US$ 7,000 daily over the course of the week with Indo rounds closing above US$ 8,500 daily. Handysize rates were reported as extremely buoyant on the northbound run with delivery Southeast Asia to NoPac rising by almost US$ 750 week-on-week (basis 38-42,000 dwt) to exceed the US$ 8,000 line.

For exclusive news and updates about dry bulk shipbroking, subscribe to the BMTI Daily Report.

The fall in spot freights has, by all signs, accelerated over the course of July with owners no longer able to depend on securing last-done levels save the very rarest of special agreements. The seasonal culprits of holiday-driven demand drift and a wider slowing in manufacturing operations that fuel that demand are both gaining force to combine into a bearish vortex that are putting charterers in the driver’s seat and owners on the sidelines. While week-on-week discounts have yet to exceed EUR 0.5/mt on any observed trade route, this is still an expanding average differential when compared to the EUR 0.25/mt limit seen until just a few weeks ago. Westward-bound freights from the Baltic States to ARAG have fallen into the EUR 21-23/mt range after trading in the EUR 22-24/mt range at the end of June and as much as EUR 25-28/mt in the first quarter of the year.

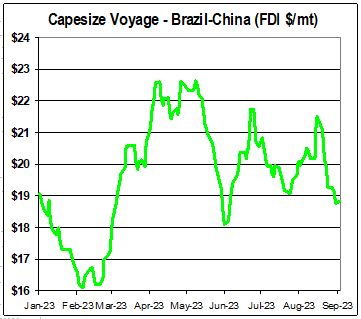

Even with the ECSA still providing just enough cargo demand to keep Brazil/China voyages hovering at US$ 20.8/mt, Capesize freights are looking at an increasingly thin upside with charterers and owners coming to something of an impasse. Pacific round voyages are also holding to circa US$ 8.2/mt, but owners are struggling to push those levels any higher for mid-July positions. Pac round time charters are under pressure in the US$ 13,000s range.

Atlantic Panamaxes are at something of an equilibrium with charterers unable to push rates for TARVs any lower than US$ 6,500 while owners are hoping to keep them above US$ 7,000 daily at the same time. South America remains the great hope to turn things around and despite continued strength from the ECSA export market, the rest of the Atlantic is far less inspiring. New front haul business is also seen stabilizing with Kamsarmaxes said to be securing upwards of US$ 15,000 daily plus US$ 500,000 BB.

Chinese holidays are probably the biggest story in the eastern Supramax trades, although they don’t seem to have subdued rates as much as they have activity with standard NoPac rounds on 58,000 dwt ships having remained largely unchanged over the past week in the US$ 7,000s. Ultramaxes are heard to be securing over US$ 8,000 on inter-Pac rounds from Singapore-Japan into SE Asia as avails tighten. Handysize activity has notably fallen off in recent days even as spot freight levels have come under the kinds of discounts that are not normally assumed to hit the small size sector with northbound rates ex-SE Asia to NoPac losing US$ 300-400 week-on-week.

For exclusive news and updates about dry bulk shipbroking, subscribe to the BMTI Daily Report.

The condition of the French soft wheat crop is its best in over a decade, says national agricultural agency FranceAgriMer. The agency says about 93% of the crop is in “good or excellent” condition compared to just 69% measured at this time last year and also the highest level since measurements began in 2011.

Prices for thermal coal worldwide have been stabilizing at around US$ 200/mt or less than half of last year’s record of circa US$ 440/mt reached in Q3 of 2022 (basis Newcastle). Observers note that present spot market prices are nonetheless more than twice the ten-year average for seaborne thermal coal before Russia’s invasion of Ukraine (US$ 86/mt).

Owners of Capesize tonnage continue to insist that enquiry is high and charterers are putting in new orders despite the fact that average rates continue to slide across the board. Whether the corrections will persist into the week ahead remains to be seen, but a stronger wave of demand would be needed to soak up the plentiful avails that are awash in both hemispheres, presenting challenges to owners who were hoping to lock in some last-minute business before the summer months start to bring a lull in earnest.

Lo and behold, it would appear that Panamax trends are starting to stabilize on the day-to-day spot market. Or at least the beginning of the week saw daily declines slow to a trickle in both hemispheres as TARVs steadied in the US$ 9,000s and front haul trips seemed to have lost the desire to drift below US$ 19,000 daily. There are even a few rumours of new demand in Southeast Asia, pushing rates into modest positivity based on early June positions. Indo rounds on Kamsarmaxes are in the US$ 8,000s.

Holidays here and holidays there (not to mention the odd historic coronation in between) are putting the brakes on business activity to a notable degree across the North Sea and, to a less extent, the Baltic market as well. Coaster trades are nonetheless more stable than one might expect them to be at this juncture with week-on-week losses looking rather minimal. On the other hand, compared to this time a year ago, rate levels have declined rather steadily and unrelentingly in the past 12 months with inter-Baltic westward freights now in the low EUR 20s/mt (basis general cargoes of 5,000mt) whereas the same business was fetching mid-high EUR 30s/mt in May of 2022. Admittedly, this was at extraordinarily high levels compared to the historical average, benefiting from the remainder of positive market vibes from the mighty upsurge of 2021. But this year’s nominal return to normality has not been as brutal as many predicted it might be. Baltic-based short sea owners are still making profits from their agreements even if earnings are nothing like they were 1-2 years ago. Northbound freights from the GNS are fetching mid-EUR 20s/mt of up to EUR 25/mt based on Irish Sea redelivery even as they began the year trading in the EUR 30s/mt. Southbound freights fixed from the UK North Sea to the Sea of Marmara are no longer fetching EUR 50s/mt as they did a month ago, but 3,000mt generals can still get high EUR 40s/mt.

To get exclusive news and trend analysis on the European short sea markets on a weekly basis, subscribe to the BMTI Short Sea Report.