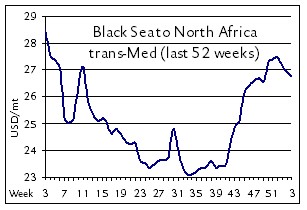

Having been pretty excited about the markets general performance, signs of a drawback are emerging. From ECSA grainhouses in all likelihood will use own tonnage to cover August cargoes. Also in the Pacific a downward correction for forward business is already obvious. The owners approach to business is always an indicator of imminent changes, in as much that dropping a trade because of charterers’ low rates, to which the owners return after they failed repeatedly elsewhere, and then being told that the business had gone. Coal shipments from India to China have almost disappeared since China has reached the quota. The next program is not expected before second half August.

As far as ECSA es concerned Ultra owners stand no chance to get any near towards US$ 15,000 daily plus 500,000ls for a fronthaul run, and given that demand is slowing rates will drop as a result. TA was done from North Brazil to Cont/Med at US$ 13,250 daily. Coastal charterers took a 28,000 dwt at US$ 7,750 daily. A 62,000 dwt was booked for a 3-5 months period at US$ 10,500 daily with redelivery Gib/Skaw range.

For shipbroking insights like this each day, subscribe to the BMTI Daily Report.

Adriatic Sea market:

Adriatic Sea market:  The holidays have continued to linger into 2020 with principals seemingly in no major rush to secure business as long as they can afford to push their requirements down the road. The unexpectedly high momentum that continued into early December and buoyed coaster markets across Europe (from north to south), remains technically in place as far as market fundamentals go, but spot freight trends are looking to move sideways at best into January with charterers expected to start applying more pressure as the month progresses. Owners remain hopeful, however, that adverse weather and their connected delays—as well as the relatively tight tonnage situation of Q4-2019—will keep things moving in their favour for at least another few weeks, but time shall tell if Baltic markets break out of their traditional cycle and do not, in fact, start to slide in January as expected. Northbound freights from the Baltic States to Ireland are fetching decent rates of EUR 30/mt, brokers say, while southbound freights from ARAG (with 5,000mt general cargoes) are securing even better rates of EUR 37-38/mt and higher. There is word, however, that charterers have already secured discounts on those levels for end-month positions.

The holidays have continued to linger into 2020 with principals seemingly in no major rush to secure business as long as they can afford to push their requirements down the road. The unexpectedly high momentum that continued into early December and buoyed coaster markets across Europe (from north to south), remains technically in place as far as market fundamentals go, but spot freight trends are looking to move sideways at best into January with charterers expected to start applying more pressure as the month progresses. Owners remain hopeful, however, that adverse weather and their connected delays—as well as the relatively tight tonnage situation of Q4-2019—will keep things moving in their favour for at least another few weeks, but time shall tell if Baltic markets break out of their traditional cycle and do not, in fact, start to slide in January as expected. Northbound freights from the Baltic States to Ireland are fetching decent rates of EUR 30/mt, brokers say, while southbound freights from ARAG (with 5,000mt general cargoes) are securing even better rates of EUR 37-38/mt and higher. There is word, however, that charterers have already secured discounts on those levels for end-month positions. [28 NOV 2019] Capital markets have not been overly enthusiastic about shipping in recent years, this past year being no exception, but, according to more than a few finance professionals, this is prime time for a turnaround in fortunes with smart money poised to see solid returns. This is also the opinion of Erik Helberg, CEO of Clarksons Platou Securities, who held a convincing presentation in Hamburg at the 23rd annual

[28 NOV 2019] Capital markets have not been overly enthusiastic about shipping in recent years, this past year being no exception, but, according to more than a few finance professionals, this is prime time for a turnaround in fortunes with smart money poised to see solid returns. This is also the opinion of Erik Helberg, CEO of Clarksons Platou Securities, who held a convincing presentation in Hamburg at the 23rd annual