A quirky Kamsarmax market in the Atlantic has given some impetus to higher rate levels. Baltic rounds are hovering around US$ 17-18,000 daily. TC trip from Black Sea to Portugal has been traded at close to US$ 20,000 daily. ECSA fronthaul runs have been done at US$ 17,500 daily plus US$ 750,000 ls. Grain charterers ex-US Gulf are holding out for US$ 50/mt for Kamsarmax stem to China. Handy activity has thrown the focus on the Continent. There is widespread view of a pretty strong market with no signs of easing yet. In an attempt to avoid high rates coal charterers decided to increase their cargo size from Handy to Kamsarmax size. Steel charterers were rating a 40,000dwt at US$ 16,000 daily from GNS to Adriatic. For a fronthaul run owners of a 29,000dwt – open in South Spain were seeing US$ 15,500 daily for a trip via St. Petersburg to the East, which on the basis of passing Skaw, would be close to US$ 20,000 daily. Black Sea grain charterers were getting rates at US$ 17.75/mt for 30,000mt from Nikatera to Egypt Med. A couple of charterers with second half October Supra stems seem be have decided to wait and keep watching the falling market for fronthaul trips. In the US Gulf period rates for 35,000dwt tonnage have been exchanged at around US$ 10,000 daily from charterers versus owners idea of US$ 12,000 daily for 12 months trading. A 61,000 dwt was tied up for a cargo from Atlantic Columbia to Brazil at the equivalent of US$ 15,000 daily, which for trips to the Med are being fixed at around US$ 21-22,000 daily. Brazil appears steadier with Ultra fronthaul rate close to US$ 17,000 daily plus US$ 685,000 ls. Coastal was done on a 36,000dwt in ballast from West Africa at US$ 17,500 daily. The East has not been too busy at all, whilst amazingly enough there is still quite a number of charterers showing interest in period tonnage.

To get exclusive and intelligent shipbroking analysis like this each and every morning, simply subscribe to the BMTI Daily Report.

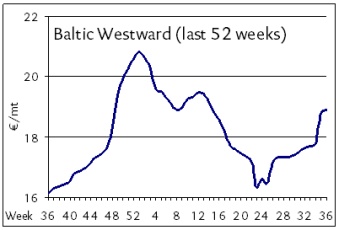

General sentiment continues to be buoyed by the ongoing grain season activities in the northern European coaster markets with new shipments entering the Baltic from Germany, Scandinavia and the Baltic States, among others. Rates have been slowly but steadily edging upward on last-done, but very slowly with some shipowners reporting week-on-week premiums of up to EUR 0.50/mt but more upgrades proving to be closer to EUR 0.25/mt if anything at all. The firming pace of activity is nonetheless expected to make September a better month than August was with hopes high across the North Sea and the Baltic Sea. Inter-Baltic trips from Norway with minor split cargoes of 3,000mt to the German Baltic continue to trade at unspectacular rates in the single digits of EUR 6-8/mt, depending on terms.

General sentiment continues to be buoyed by the ongoing grain season activities in the northern European coaster markets with new shipments entering the Baltic from Germany, Scandinavia and the Baltic States, among others. Rates have been slowly but steadily edging upward on last-done, but very slowly with some shipowners reporting week-on-week premiums of up to EUR 0.50/mt but more upgrades proving to be closer to EUR 0.25/mt if anything at all. The firming pace of activity is nonetheless expected to make September a better month than August was with hopes high across the North Sea and the Baltic Sea. Inter-Baltic trips from Norway with minor split cargoes of 3,000mt to the German Baltic continue to trade at unspectacular rates in the single digits of EUR 6-8/mt, depending on terms.