The decent handful of new TCs that came through for the Capesizes at midweek were not repeated by the end of the week, but no bother. Sentiment has been sufficiently triggered to start rising once again as the long-delayed requirements of the holiday period seem to be again entering the spot market with employment enquiries being reported by owners in the Atlantic and Pacific alike. Front hauls have been broadly upgraded with as much as US$ 23,500 daily on offer for standard tonnage from the Continent into the CJK area. Voyage rates enjoy another boost as well with Brazil/China climbing back over the US$ 15/mt marker with some owners already claiming to have US$ 16/mt on lock for end-May.

Perhaps inspired by the same gust of wind that has lifted the Capes—not to mention a new sense of purpose in the East—Panamax freights are firming a little bit faster, suggesting potential for a real recovery by next week, assuming trends hold steady. Front hauls have been getting fixed in the mid US$ 17,000s we are told, though this run is still too little frequented to make a fair assessment. Aussie rounds are pushing toward US$ 10,000 on Kamsarmaxes.

Improvements build for Supramaxes on Black Sea delivery with front hauls said to be hovering under US$ 13,000 daily on modern ships. Trans-Atlantic trades ex-USG remain problematic, but minerals on Tess 58s are securing steady rates of US$ 11,000 and up on UKC-Med redelivery with talk of US$ 11,500 on the horizon for the same business. Indo rounds are onwards and upwards with Supramax tonnage having set the new high water mark at US$ 9,500.

To read shipbroking analysis like this every day, subscribe to the BMTI Daily Report.

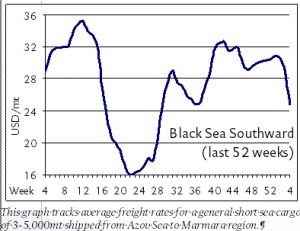

Freights continue to fall rather precipitously in the Azov trades with owners continuously coming up short on the cargo side of the market. Owners say rates have fallen so quickly since their recent peak at the end of 2018 that they are down as much as US$ 9/mt now from that point, roughly a third, considering that Azov/Marmara rates are currently in the low US$ 20s/mt on grain of 5,000mt (46′). A veritable perfect storm of bearish conditions—extended port delays at Russian ports, the stronger rouble, increased domestic commodity demand (along with lower international demand), rising domestic prices and the fairly mild winter—are conspiring to make this winter a tougher than usual one for shipowners. Kherson/TBS has stabilized at US$ 20-22/mt.

Freights continue to fall rather precipitously in the Azov trades with owners continuously coming up short on the cargo side of the market. Owners say rates have fallen so quickly since their recent peak at the end of 2018 that they are down as much as US$ 9/mt now from that point, roughly a third, considering that Azov/Marmara rates are currently in the low US$ 20s/mt on grain of 5,000mt (46′). A veritable perfect storm of bearish conditions—extended port delays at Russian ports, the stronger rouble, increased domestic commodity demand (along with lower international demand), rising domestic prices and the fairly mild winter—are conspiring to make this winter a tougher than usual one for shipowners. Kherson/TBS has stabilized at US$ 20-22/mt. Some of the shine is already off of the

Some of the shine is already off of the